Current State of Steel Demand in Europe: A Slow Path to Recovery

The European steel industry is set for a modest recovery in 2025, bolstered by improved demand from the manufacturing sector, a rebound in construction activities, and pent-up demand. According to Fitch Ratings, eased financing conditions and falling raw material costs are expected to drive a slight improvement in steel margins, although structural challenges persist.

According to GMK Center, the European Union is facing a prolonged struggle to revive its industrial and economic sectors, particularly the construction and steel markets, amidst challenging macroeconomic conditions. With its position as Ukraine’s largest trading partner, Europe’s economic health is critical not only for its own growth but also for Ukraine’s iron and steel exports.

Ukraine’s Reliance on the European Market

Ukraine has increasingly relied on the European Union as its primary trading partner during the ongoing war. The lifting of trade restrictions and Europe’s geographical proximity have facilitated this shift. In the first half of 2024, Ukrainian exports to the EU accounted for 56% of the country’s total exports, equaling $11 billion.

The importance of Europe is particularly pronounced in Ukraine’s steel sector, where 84% of steel exports in the first half of the year went to European countries. Consequently, Ukraine’s iron and steel sector is intricately tied to the health of the EU market.

Macroeconomic Challenges in Europe

The European economy continues to grapple with the fallout of multiple crises over the past few years. The shockwaves of Russia’s aggression in 2022 disrupted supply chains, drove energy prices to record highs, and set the stage for inflationary pressures. In 2023, the EU economy managed only a meager 0.4% growth compared to 3.4% the previous year, reflecting reduced industrial activity.

Economic Growth: Uneven Recovery

Eurozone GDP grew by just 0.3% in the second quarter of 2024 compared to the first quarter. However, growth has been uneven among major economies. For instance:

- Germany’s GDP declined by 0.1%.

- France, Italy, and Spain saw growth of 0.3%, 0.2%, and 0.8%, respectively.

While the collective growth of other countries has offset Germany’s decline, the overall business climate remains pessimistic. Indicators such as the Economic Sentiment Index stood at a low 96.6 points in August.

Interest Rates and Inflation

The European Central Bank (ECB) has been attempting to stabilize inflation by adjusting interest rates. A slight reduction in June 2024 saw rates drop by 25 basis points, with expectations of further cuts later in the year. However, the impact of these measures will take time to reflect in improved credit conditions and industrial activity.

European Steel Market: Demand Trends

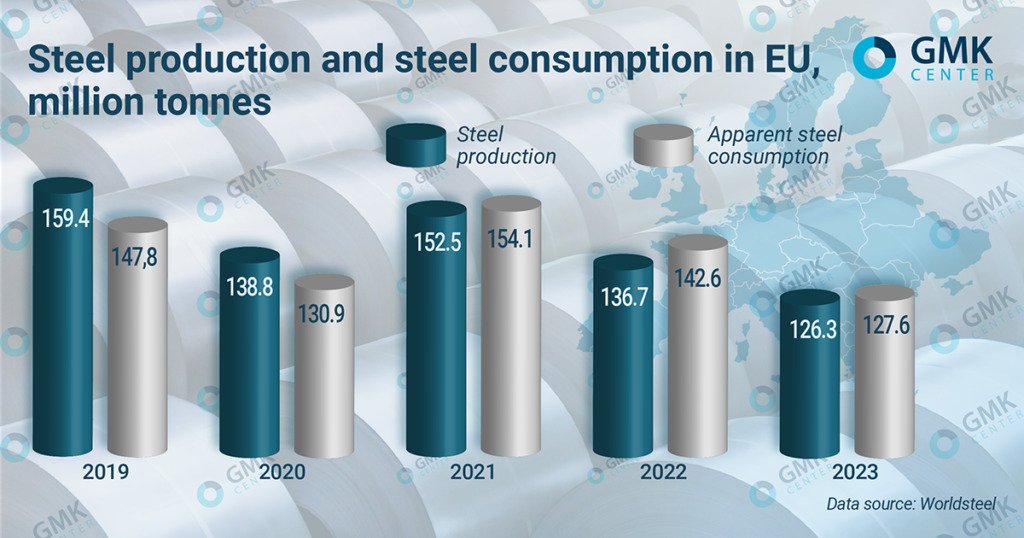

The European steel market remains under pressure, with weak demand influenced by geopolitical, economic, and energy-related challenges. According to EUROFER, steel consumption in the EU is expected to grow by a modest 1.4% in 2024 after an 8.7% decline in 2023.

This “technical rebound” will still fall short of restoring pre-crisis levels. A more meaningful recovery is projected for 2025, with apparent steel consumption anticipated to rise by 4.1%, reaching 133 million tons.

Key Steel-Consuming Sectors: Current Challenges and Prospects

1. Construction Sector

As the largest consumer of steel in the EU (33% of total demand), the construction industry has been heavily impacted by rising material costs, labor shortages, and tightened credit availability.

- In 2023, construction activity declined by 1%.

- A further decline of 1.4% is expected in 2024 due to reduced government support.

On a brighter note, eased monetary policies and better financing conditions in 2025 are expected to drive a 1.8% increase in construction activity.

2. Automotive Industry

Accounting for 18% of total steel consumption, the automotive sector experienced a rebound in 2023 with an 8.7% growth in production. However, the sector’s recovery remains fragile due to declining car registrations in key markets (Germany, France, and Italy) and uncertainty over electric vehicle (EV) standards.

- A 3% decline in automotive production is forecast for 2024.

- A rebound of 2.3% is projected in 2025, spurred by improving economic conditions and policy clarity around EV infrastructure.

3. Engineering and Machinery

The engineering sector, responsible for 14% of EU steel consumption, has faced significant challenges from high energy prices and reduced manufacturing activity.

- Growth in engineering slowed to 2.6% in 2023, down from 5.7% in 2022.

- A 1.9% contraction is expected in 2024, with recovery anticipated only in 2025 (+2.1% growth).

Cautious Optimism: Drivers of Recovery

Despite the current challenges, there are reasons to remain cautiously optimistic about the European economy and steel market recovery:

- Improved Credit Conditions:

The ECB’s interest rate cuts are expected to gradually lower borrowing costs, stimulating industrial and consumer spending by mid-2025. - Increased Infrastructure Investments:

As the EU focuses on green transition projects such as renewable energy installations and EV infrastructure, demand for steel is expected to rise. - Export Opportunities for Ukraine:

A stronger EU economy will benefit Ukrainian steel exports, provided trade restrictions remain lifted and mechanisms like CBAM (Carbon Border Adjustment Mechanism) are adjusted to accommodate Ukrainian exporters. - Shift Toward Sustainability:

Steelmakers investing in sustainable production processes, such as hydrogen-based steelmaking and increased recycling, are likely to gain a competitive edge in the evolving market landscape.

Challenges to Long-Term Growth

- Geopolitical Risks:

Escalating hostilities in Ukraine or broader geopolitical tensions could disrupt recovery efforts. - Labor Market Pressures:

A shortage of skilled labor in construction and manufacturing poses a risk to production capacities. - Dependence on Green Transition Investments:

While green initiatives are essential for long-term sustainability, their high upfront costs and uncertain returns may strain national budgets and private investments. - Global Competition:

The European automotive sector faces growing competition from Chinese EV manufacturers, which could limit its recovery and steel demand.

Factors Driving Recovery in Steel Demand

- Infrastructure Investments:

The European Union is poised to ramp up infrastructure spending to meet green energy and sustainability goals. Initiatives such as wind turbine installations, electric vehicle infrastructure, and sustainable building projects will boost steel consumption. - Automotive Sector Revival:

The automotive industry, a major steel consumer, is showing signs of recovery. Increased production of electric vehicles (EVs) is particularly promising, as these vehicles require significant amounts of advanced, lightweight steel for battery casings and structural components. - Energy Transition Goals:

Europe’s focus on renewable energy and grid modernization involves significant steel usage. Solar panel installations, offshore wind farms, and hydrogen pipelines will drive demand for specialized steel grades. - Improved Global Supply Chains:

After the disruptions caused by the COVID-19 pandemic, global supply chains are gradually stabilizing. This will enable European steelmakers to secure raw materials more efficiently and meet increasing demand.

Steel Demand Trends

The European Steel Association (Eurofer) forecasts a 0.6% recovery in EU steel demand in 2025. Despite this, overall consumption will remain below pre-pandemic levels. The decline in real steel demand, which has been ongoing since 2017 (excluding a brief post-COVID-19 recovery in 2021), reflects the challenges faced by the sector.

- Demand Decline: Real steel demand decreased by 1.4% in 2023 and is projected to decline by an additional 3% in 2024.

- Contributing Factors: Weak demand in construction and automotive sectors, geopolitical uncertainties, persistent conflicts, monetary tightening, inflation, and elevated energy prices have all played significant roles in this downturn.

Construction and Automotive Sectors

The construction and automotive industries, two critical steel-consuming sectors, have been under immense pressure:

- Construction: Rising costs, labor shortages, and reduced government support have constrained growth. However, eased financing conditions in 2025 are expected to unlock new opportunities, leading to a gradual recovery in the sector.

- Automotive: The sector faces stagnation due to low consumer confidence, uncertainty around electric vehicle regulations, and competition from non-European manufacturers. This has led to a prolonged slump in demand.

Improved Margins for Producers

Margins for European steel producers have been under pressure due to structural weaknesses in the domestic market, with the exception of a temporary boost during the post-COVID recovery period. In 2025, a slight rebound in steel prices and reduced raw material costs are expected to provide some relief.

International Trade Impact

Steel exports from the EU have remained a critical component of the market, with the United States being the second-largest destination, accounting for 14% of exports in 2023. The exemption of EU steel exports from US Section 232 tariffs has provided some relief. However, potential trade measures introduced by the new US administration could have far-reaching implications, depending on their scope.

Future Prospects and Challenges

The modest recovery in 2025 is expected to be driven by:

- Improved credit availability.

- Stabilization in energy prices.

- A rebound in demand across key sectors, including construction and manufacturing.

However, the industry continues to face structural challenges, including:

- Persistent geopolitical tensions.

- Limited innovation in growth-driving sectors.

- High inflationary pressures.

Steel and the Push for Sustainability

Sustainability is becoming a central theme in the steel industry’s future. European steelmakers are under pressure to reduce carbon emissions and transition to greener production methods.

Key Sustainable Innovations in Steelmaking Include:

- Hydrogen-based Steelmaking: Using green hydrogen as a reducing agent in place of coal.

- Circular Economy Practices: Recycling scrap steel to minimize waste and reduce energy consumption.

- Energy Efficiency Upgrades: Investing in technologies that lower the energy intensity of production processes.

The transition to sustainable steelmaking aligns with the European Green Deal, which aims to achieve net-zero carbon emissions by 2050.

Opportunities for Growth in the European Steel Market

While challenges persist, the European steel industry is well-positioned to capitalize on emerging opportunities:

- Advanced High-Strength Steel (AHSS):

Growing demand for AHSS in the automotive and aerospace sectors presents a significant growth avenue. AHSS offers high strength and durability while reducing weight. - Collaborations and Innovations:

Partnerships between steelmakers and technology providers can accelerate the development of innovative solutions, such as AI-driven process optimization and predictive maintenance. - Expansion into New Markets:

European steelmakers can diversify their customer base by exploring opportunities in developing regions that are rapidly industrializing.

Conclusion: A New Era for European Steel

While 2025 offers a glimmer of hope for the European steel industry, the recovery is expected to be marginal and constrained by long-standing challenges. Addressing structural inefficiencies, fostering innovation, and managing external trade dynamics will be crucial for sustainable growth in the years ahead.

The sector’s performance will largely depend on broader macroeconomic conditions, the resolution of geopolitical tensions, and policies supporting industrial growth.

Sustainability will be a defining factor, as steelmakers embrace greener technologies to align with global environmental goals. By leveraging technological innovations and addressing market challenges, the industry can secure its long-term competitiveness.

For businesses relying on high-quality steel products and services, staying ahead of these trends is essential. At Lux Metal Group, we are committed to delivering premium steel solutions tailored to your needs.

References: