Sale of US Steel Kicks Up a Political Storm

Once the heart of American industry, Pittsburgh earned its moniker “Steeltown USA” through generations of steel production. The city’s historic blast furnaces and legendary football team, the Steelers, symbolized a robust working-class culture powered by the steel industry. But times have changed.

Now, the potential sale of U.S. Steel to Japan’s Nippon Steel Corp. has sparked controversy that extends far beyond Pennsylvania. In an election year, this acquisition has become a political flashpoint — with both U.S. President Joe Biden and former President Donald Trump publicly opposing the foreign takeover.

What’s Really at Stake?

While U.S. Steel no longer holds the industrial dominance it once had, the company remains a symbolic pillar of America’s industrial identity. It ranked just 27th in global steel production in 2023, according to the World Steel Association, yet its brand carries immense political and emotional weight, particularly in the Rust Belt.

In Pittsburgh, the reaction is mixed. Some see the deal as an economic threat — a potential repeat of the devastating mill closures that began in the 1980s. Others, especially newer generations in the city’s tech and healthcare-dominated economy, are more concerned about the environmental toll of aging steel plants like Edgar Thomson Works, the last operating blast furnace in the region.

Why Is There Political Backlash?

The United Steelworkers union opposes the sale, and both Biden and Trump have voiced their intent to block it. Their concerns are twofold: the national security implications of foreign ownership of critical infrastructure, and the economic symbolism of surrendering a historic American steelmaker.

The Committee on Foreign Investment in the United States (CFIUS) is currently reviewing the deal, with the Department of Justice also conducting an antitrust evaluation. Politicians from both parties — from progressive Democrats like John Fetterman to conservative Republicans like J.D. Vance — have united in opposition.

At the heart of the matter is a shared concern: will foreign ownership mean fewer American jobs, or perhaps another wave of deindustrialization?

Nippon Steel’s Strategy: Reassure, Reinvest, Rebrand

Nippon Steel has launched an aggressive public relations campaign, promising to preserve jobs and relocate its U.S. headquarters to Pittsburgh. The company says it will invest in modernizing outdated steel plants and keep the U.S. Steel name alive.

But skepticism remains. Despite these reassurances, residents remember past mill closures that devastated communities. Local stakeholders fear history may repeat itself.

Pittsburgh: From Steeltown to Innovation Hub

The reality is that Pittsburgh has already moved on from its steel-dominated past. Once a chain of blast furnaces along the Monongahela River, the city is now known more for its universities, hospitals, and burgeoning tech sector than for molten metal.

Today, steel jobs in the region number around 5,000 — a fraction of what they were in their prime. The environmental costs of steelmaking have become a greater concern for younger residents. Activists and local progressives point to air pollution and climate change as reasons to phase out legacy industries like coal-based steel production.

Still, for towns surrounding Pittsburgh — many of which never recovered from steel’s decline — the fear of further economic displacement is real and immediate.

A Broader Trend in Global Steel

The U.S. Steel sale is just one part of a broader reshuffling of the global steel landscape. Protectionist tariffs, like the 25% import duties reintroduced in 2024, have sparked a rise in domestic investment and international tension. Foreign companies, like Hyundai and Johnson & Johnson, are now planning massive U.S.-based production facilities to avoid such tariffs — a strategy Nippon Steel is likely emulating with this acquisition.

As the global steel industry continues to evolve, alliances, national interests, and industrial policy will increasingly shape the market — often more than pure economics.

A Vicious Circle of Tariffs and Price Inflation

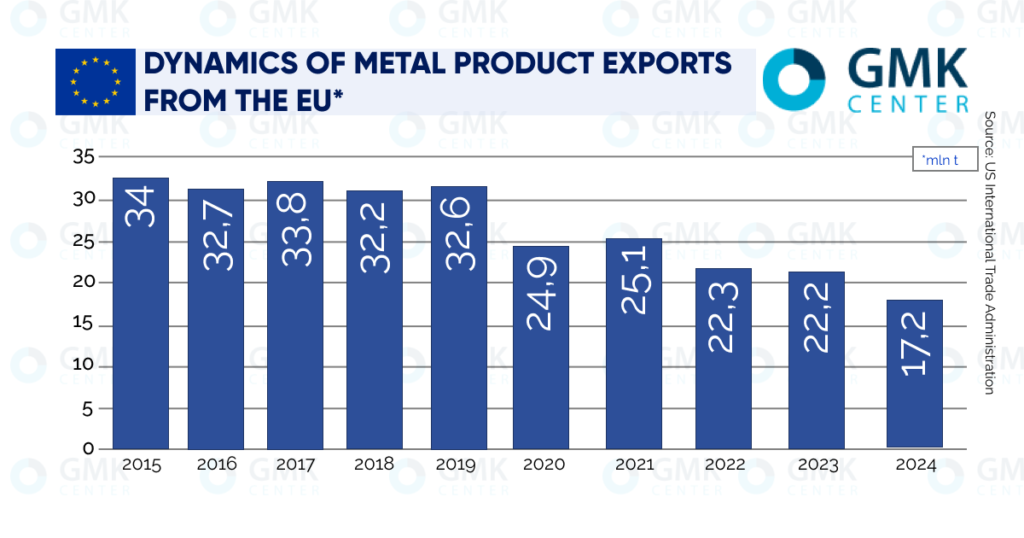

The 25% steel import duty is not new. It first appeared in 2018 under President Donald Trump, and though President Joe Biden eased the measure in 2021 by establishing a quota of 3.3 million tons annually for EU imports, this did little to reinvigorate metal exports from Europe.

By 2024, however, EU-to-U.S. steel exports rebounded strongly—rising 45% compared to 2019, reaching €8 billion in value. But this comeback is now under threat with the reinstatement of full tariffs.

While these protectionist policies are meant to shield U.S. industries from lower-cost foreign steel, they often backfire. World Steel Dynamics notes that the price differential between the U.S. and EU is over 55%, which still makes exports viable even with the 25% tariff—for now.

Yet, there’s a catch: consumer demand. If it weakens, high prices won’t last, import interest will wane, and U.S. steelmakers may need to lower expectations.

Automotive Sector: Tariff Fallout Begins

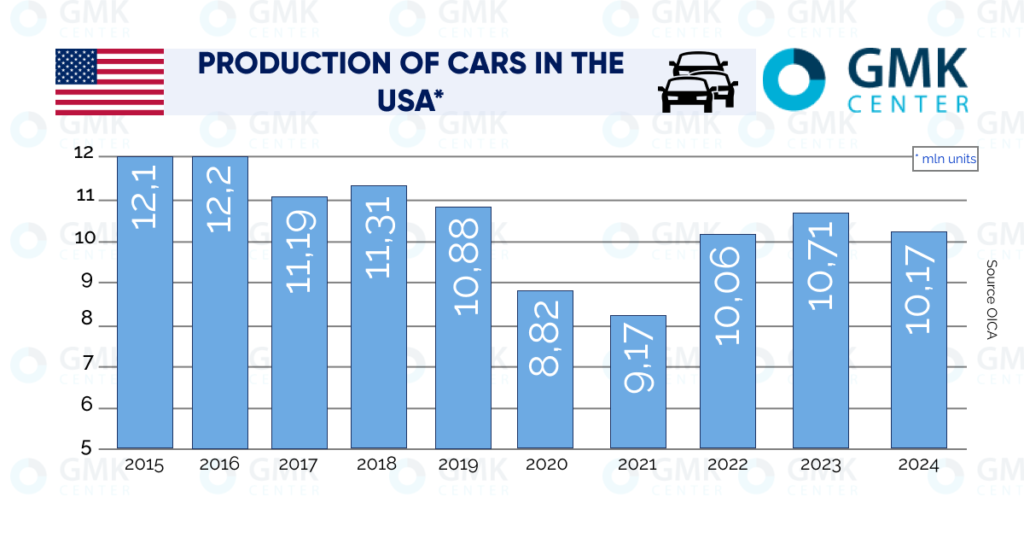

The U.S. automotive industry, once a key driver of steel demand, is now under pressure. Car sales have struggled to return to pre-pandemic levels. In early 2025, sales dropped by 3.1% year-over-year, and further disruptions are expected due to a separate 25% import duty on all cars and spare parts taking effect no later than May 3.

While labor unions praise the move for protecting American jobs, automakers are warning of cost surges. According to Cox Automotive, vehicles assembled in the U.S. could become $3,000 more expensive, while those from Canada or Mexico could rise by $6,000.

This will hurt demand—and steel consumption. Moreover, U.S. car exports have plummeted from 4.3 million units in 2014 to just 1.43 million in 2024, with retaliatory tariffs from the EU and China expected to reduce exports even further.

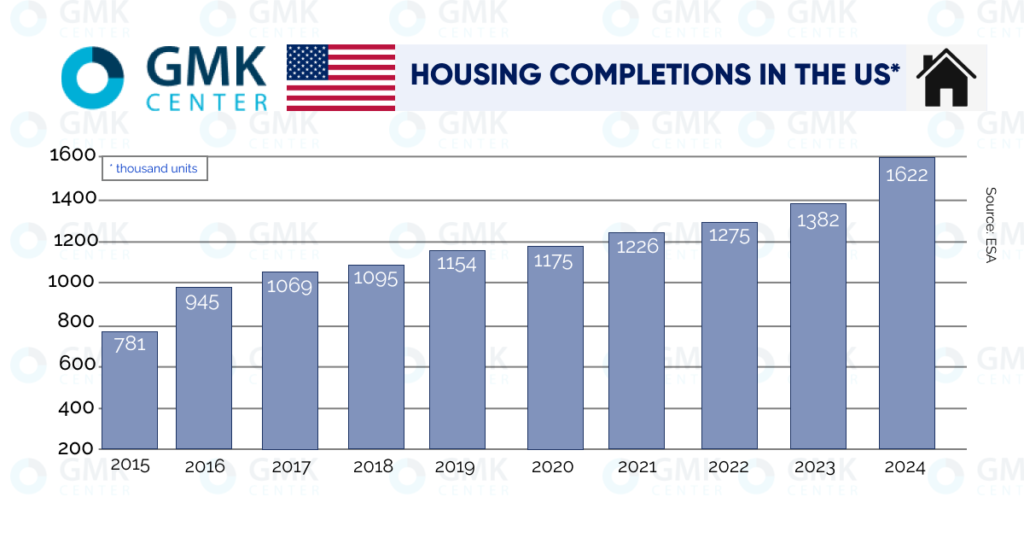

Construction: A Beacon of Growth for Steel Demand

While automotive steel use softens, U.S. construction remains a promising growth area, especially residential and industrial building:

- Housing Starts: 2024 saw a 5.9% increase, and 2025 projections suggest 14% growth—driven by more compact and affordable housing.

- Mortgage Rate Impact: With expected rate cuts by the U.S. Federal Reserve, the housing market could accelerate further if inflation is kept in check.

- Infrastructure Boom: The $550 billion U.S. Infrastructure Investment and Jobs Act is funding a nationwide overhaul through 2027, with projects in energy, transportation, and broadband—fueling steel demand.

- Green Energy Construction: From 2024–2027, the U.S. will add nearly 100 GW of solar and 23 GW of wind power capacity, driving demand for structural steel and support systems.

Industrial Construction: Foreign Giants Move In

In a twist of irony, U.S. protectionist policies are compelling global corporations to “build local”:

- Hyundai is investing $5.8 billion in a Louisiana steel plant with a capacity of 2.7 million tons/year to bypass duties.

- TSMC plans to spend $100 billion on chip fabs in Arizona, with the first plant launching in 2028.

- Johnson & Johnson and Eli Lilly are together investing over $80 billion to expand pharmaceutical manufacturing within U.S. borders by 2030.

This strategic onshoring trend not only supports American steel consumption but also reflects a global shift in production strategy—one that’s increasingly driven by politics as much as economics.

What This Means for Global and Malaysian Steel Businesses

For exporters and manufacturers like Lux Metal, the U.S. market is becoming increasingly difficult to access. Yet, the price premium and persistent demand in U.S. construction offer limited—but valuable—opportunities, especially for value-added products or partnerships with onshore builders.

Meanwhile, this global shift toward regionalized manufacturing could open up new avenues for ASEAN producers to step in where EU suppliers are blocked—or to support local assembly for U.S.-bound components.

As international trade realigns, we remain focused on providing flexible, customized steel solutions, supporting clients across industries—from construction to renewable energy—with precision, quality, and reliable delivery.

New U.S. Tariffs Disrupt EU Steel Market – Recovery Delayed Until 2026

The European steel industry, already grappling with sluggish demand and economic uncertainty, is facing yet another major challenge: the United States’ decision to double tariffs on steel imports to 50%. This significant policy move is expected to disrupt global trade flows and worsen the EU’s steel consumption outlook.

A Fourth Year of Decline for European Steel

According to the latest EUROFER (European Steel Association) forecast, what was once anticipated as a recovery year for the EU steel market in 2025 has now been revised to show further contraction. EUROFER predicts a 0.9% drop in steel consumption in 2025, following a 1.1% decline in 2024—marking four consecutive years of market shrinkage.

While the broader European economy shows some resilience in the service sector, the industrial base—especially steel-intensive sectors like automotive and construction—continues to weaken. In 2024, steel consumption saw a marginal increase in Q4 (+0.5%) to reach 30.1 million tonnes, but domestic supply declined by 2%, and imports soared to a record-high 27% market share.

EUROFER’s CEO Axel Eggert noted, “The new U.S. duties are another blow to the EU market, already suffering from global overcapacity, high energy prices, and geopolitical instability. Producers are being forced to halt production, lay off workers, and delay key decarbonization initiatives.”

Steel-Consuming Sectors Under Pressure

The automotive sector—a key consumer of steel—contracted by 2.6%, while the construction sector also reported significant setbacks. In 2025, EUROFER expects another 0.5% drop in the Steel Weighted Industrial Production (SWIP) index, which reflects the performance of steel-consuming industries. Only by 2026 is a recovery (+1.3%) expected.

With the 50% U.S. import duty effectively pricing out many foreign steel suppliers, EUROFER warns that cheap steel originally destined for the U.S. may now flood the European market, unless the European Commission acts swiftly with countermeasures.

Understanding the U.S. Steel Market and Economy

The decision to impose a 50% import tariff on steel is part of a broader protectionist agenda aimed at shielding U.S. industries and encouraging domestic production. This follows a pattern of trade barriers first implemented in 2018 under the Trump administration, which originally set tariffs at 25%. The latest increase to 50% sends a strong signal: the U.S. is determined to restrict foreign competition in key industrial sectors.

Here are key factors shaping the U.S. steel market and economy in 2025:

1. Domestic Steel Demand Remains High

The U.S. continues to experience robust demand from construction and infrastructure development, largely fueled by the $550 billion Infrastructure Investment and Jobs Act. Government funding has accelerated projects across transportation, energy, and utilities—driving significant steel consumption in these sectors.

Additionally, industrial construction is rising due to strategic investments by multinational companies building plants in the U.S. to avoid tariffs. Projects like Hyundai’s new steel plant in Louisiana and TSMC’s semiconductor facility in Arizona represent long-term commitments to U.S. domestic manufacturing.

2. Automotive Sector Facing Headwinds

While automotive production in the U.S. is recovering, it’s not without issues. New 25% tariffs on imported cars and spare parts could lead to higher vehicle prices, discouraging consumer purchases and dampening demand for auto-grade steel. Moreover, the U.S. auto export market has shrunk dramatically over the past decade, further weakening global steel demand from this sector.

3. Inflationary Pressure and Policy Uncertainty

Rising tariffs, including those on steel and automotive goods, have contributed to inflationary pressure. While the U.S. Federal Reserve aims to lower interest rates in 2025 to stimulate the economy, persistent inflation could delay policy shifts. As a result, uncertainty in consumer spending and business investment may continue.

Conclusion: A Legacy in Transition

The U.S. steel market is becoming increasingly self-contained, driven by protectionist policies and government-led industrial expansion. While this may benefit domestic steel producers, it complicates matters for global exporters—including those in the EU—who now face limited access, displaced trade flows, and fierce price competition.

At Lux Metal, we continue to monitor these developments closely. We remain committed to supporting clients with adaptive strategies, competitive custom metal solutions, and a deep understanding of global steel dynamics—whether in Europe, North America, or Southeast Asia.

As the market evolves, proactive innovation, flexible supply chains, and local partnerships will be essential in navigating this changing global steel landscape.

The U.S. Steel–Nippon Steel deal reflects more than a business transaction — it’s a cultural flashpoint in America’s ongoing debate over industry, identity, and the global economy. As a company focused on precision steel manufacturing, LUX METAL continues to monitor these global developments closely.

The story of Pittsburgh is a powerful reminder: while markets and technology change, the human and emotional ties to steel endure. As the industry shifts toward cleaner, more localized, and more diversified production, we must remember that every transition brings both opportunity and challenge — and companies that adapt thoughtfully will lead the way.

About LUX METAL

LUX METAL is a leading Malaysian steel manufacturer offering customized metal solutions tailored to various industry needs. We specialize in stainless steel fabrication, laser cutting, precision bending, welding, CNC machining, and more — delivering top-quality results backed by modern technology and craftsmanship.

🔗 Visit us at: www.luxmetalgroup.com