The Surge in Steel Imports

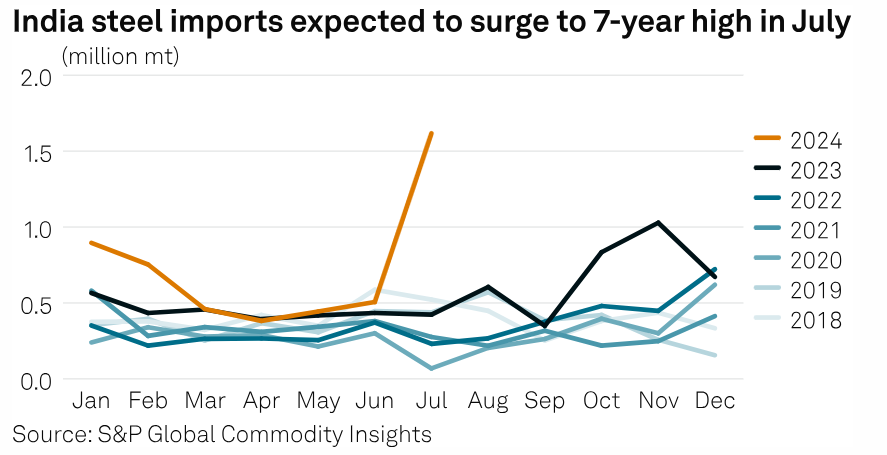

According to government data, India imported 5.7 million metric tons of finished steel during April–October 2024, marking a seven-year high. This increase has been driven by several factors:

1. China’s Dominance as a Supplier

China is the largest supplier of rolled steel to India, leveraging its surplus production to offer competitive prices. Cheap imports from China, Japan, South Korea, and Vietnam have found a strong foothold in India’s market.

2. Rising Demand in Key Sectors

India’s domestic demand for steel, particularly from the automotive and infrastructure sectors, reached a record high of 85.7 million tons during the same period. However, a significant portion of this demand is being met by cheaper foreign imports.

3. Shift in Trade Dynamics

Interestingly, Vietnam, previously a buyer of Indian steel, has now emerged as an exporter, further increasing the competition for Indian manufacturers.

4. Declining Exports

While imports surged, India’s steel exports hit a seven-year low of 2.8 million tons during April–October 2024, falling sharply by 35.9% year-on-year. The declining export trend has compounded challenges for domestic steelmakers.

Impacts on India’s Steel Industry

The influx of cheap imports has created a host of challenges for India’s steelmakers, forcing them to reevaluate strategies and seek government intervention.

1. Erosion of Profit Margins

India’s steelmakers, including giants like JSW Steel and Tata Steel, have reported a dramatic loss in margins, ranging from 68% to 91% in 2024/25. The flood of low-cost imports has pressured domestic prices, eroding profitability and deterring investors.

2. Declining Market Share

The domestic industry’s share in segments such as hot-rolled steel (17%), coated steel (20%), and plates (19%) has been displaced by cheaper Chinese, Japanese, and South Korean imports.

3. Threat to Capacity Expansion

With margins plummeting and funding drying up, expansion projects have stalled, jeopardizing the industry’s growth trajectory.

4. Regional Trade Shifts

Vietnam, which was once a key export destination for Indian steel, is now competing directly with India, highlighting the shifting landscape of regional steel trade.

China Takes the Lead in India’s Steel Imports

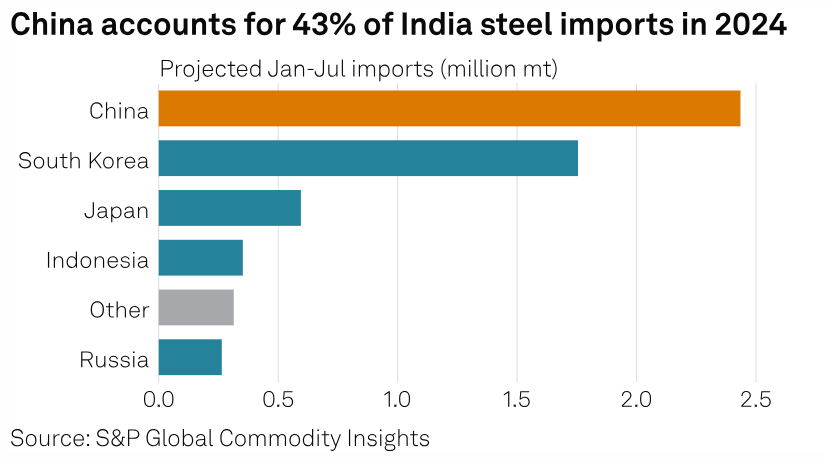

From January to July 2024, China surpassed South Korea to become the largest steel exporter to India, contributing 43% of India’s total steel imports. South Korea accounted for 31% during the same period.

This trend culminated in July, with Chinese steel expected to comprise a staggering 73% of total imports. This surge was fueled by contracts signed between late May and early June, during a period of declining Chinese steel prices and relatively high domestic hot-rolled coil (HRC) prices in India, which stood at INR 54,000 per metric ton.

A Chinese exporter remarked, "Current bids from India are too low; we can't command any premium compared to other regions, but it's better than nothing." Such sentiments highlight how competitive pricing has driven China's export growth to India.

Vietnam Joins the Race

Vietnam has also emerged as a significant player in India’s steel market. Formosa Ha Tinh Steel, a Vietnamese mill that acquired BIS certification for HRC exports in July, became a competitive force, offering HRC at $560/mt CFR Mumbai and $553/mt CFR Chennai. Chinese HRC, meanwhile, was priced slightly lower at $540-$545/mt CFR India. However, the 7.5% import duty on Chinese steel narrowed the competitiveness gap, making Vietnamese offers more attractive in certain cases.

The Domestic Steel Market Under Pressure

India’s domestic steel market faces challenges as imported steel products increasingly undercut local prices. For instance, Chinese cold-rolled coil (CRC) imported at $610/mt was INR 4,000 per metric ton cheaper than domestically produced CRC, even after factoring in a 7.5% import tariff. This price disparity is squeezing Indian manufacturers, who are already grappling with subdued export demand.

Additionally, declining demand in Italy and other export markets has compounded the challenges for Indian steelmakers. In July, Japanese imports were priced at INR 51,000/mt ex-stock Mumbai, making domestic ex-works prices uncompetitive.

China Leads Surge in India’s Steel Imports: Unraveling the Dynamics

India’s steel import market has experienced a notable shift in 2024, with China emerging as the dominant supplier amidst a surge in steel imports. The combination of competitive pricing, strategic supply deals, and rising domestic demand has positioned China as a key player in India’s steel industry. This blog delves into the factors driving this surge, the implications for India’s domestic market, and the challenges faced by Indian steelmakers.

China Takes the Lead in India’s Steel Imports

From January to July 2024, China surpassed South Korea to become the largest steel exporter to India, contributing 43% of India’s total steel imports. South Korea accounted for 31% during the same period.

This trend culminated in July, with Chinese steel expected to comprise a staggering 73% of total imports. This surge was fueled by contracts signed between late May and early June, during a period of declining Chinese steel prices and relatively high domestic hot-rolled coil (HRC) prices in India, which stood at INR 54,000 per metric ton.

A Chinese exporter remarked, “Current bids from India are too low; we can’t command any premium compared to other regions, but it’s better than nothing.” Such sentiments highlight how competitive pricing has driven China’s export growth to India.

Vietnam Joins the Race

Vietnam has also emerged as a significant player in India’s steel market. Formosa Ha Tinh Steel, a Vietnamese mill that acquired BIS certification for HRC exports in July, became a competitive force, offering HRC at $560/mt CFR Mumbai and $553/mt CFR Chennai. Chinese HRC, meanwhile, was priced slightly lower at $540-$545/mt CFR India. However, the 7.5% import duty on Chinese steel narrowed the competitiveness gap, making Vietnamese offers more attractive in certain cases.

The Domestic Steel Market Under Pressure

India’s domestic steel market faces challenges as imported steel products increasingly undercut local prices. For instance, Chinese cold-rolled coil (CRC) imported at $610/mt was INR 4,000 per metric ton cheaper than domestically produced CRC, even after factoring in a 7.5% import tariff. This price disparity is squeezing Indian manufacturers, who are already grappling with subdued export demand.

Additionally, declining demand in Italy and other export markets has compounded the challenges for Indian steelmakers. In July, Japanese imports were priced at INR 51,000/mt ex-stock Mumbai, making domestic ex-works prices uncompetitive.

Government Support Sought by Indian Mills

Indian steelmakers, including giants like AM/NS India and JSW Steel, have urged the government to take protective measures against the influx of cheap imports from China and Vietnam.

Dilip Oommen, CEO of AM/NS India, stated, “We remain hopeful that the government will take decisive actions to curb steel imports at predatory prices, which is a serious and immediate concern.”

Despite these appeals, the government did not announce any safeguard measures during the Union Budget on July 23. However, the industry remains optimistic about potential interventions, especially given the rising volume of imports from China.

Competitive Pressures from Japan and South Korea

While China dominates, Japan and South Korea remain strong competitors. South Korea, previously the largest exporter to India, accounted for 45% of imports in 2023. Weak domestic demand in South Korea and a depreciating yen in Japan have made their steel exports more competitive.

Leading exporters such as POSCO, Hyundai Steel, JFE, and Nippon Steel have intensified their presence in the Indian market. For September deliveries, Japanese HRC was offered at $580/mt CFR India, reflecting the competitive environment Indian steelmakers must navigate.

Implications for India’s Steel Industry

The surge in imports and the associated price pressures pose several challenges for India’s steel industry:

- Market Share Loss: Imported steel, priced more competitively, is eating into the market share of domestic producers. In July alone, imported steel replaced 17% of hot-rolled products, 20% of coated steel, and 19% of plate segments in India.

- Profit Margins Under Pressure: Indian steelmakers have reported significant margin declines, with some estimates suggesting a drop of 68%-91% during 2024-2025.

- Capacity Expansion Delayed: The financial strain has led to uncertainty among investors, affecting plans for capacity expansion.

The Path Forward

To address the challenges posed by rising imports, the Indian steel industry has called for government intervention, such as imposing safeguard duties or anti-dumping measures. The Directorate General of Trade Remedies (DGTR) has been engaged to investigate whether cheap steel imports are harming domestic producers. However, the implementation of protective measures will depend on the outcome of these investigations.

Strategies for Resilience

To navigate these challenges, India’s steelmakers must adopt a mix of short-term protective measures and long-term strategies to enhance competitiveness.

1. Protecting Domestic Markets

Temporary tariffs and anti-dumping duties can provide immediate relief, giving domestic players a chance to regain market share.

2. Diversifying Product Offerings

Focusing on value-added steel products can help manufacturers differentiate themselves from generic imports.

3. Emphasizing Sustainability

Investments in energy-efficient and environmentally friendly production technologies can enhance competitiveness in the long run.

4. Strengthening Export Markets

Rebuilding relationships with key export markets and exploring new opportunities in regions with high steel demand can offset domestic challenges.

5. Industry-Government Collaboration

A coordinated effort between the steel industry and government is essential to implement effective policies, foster innovation, and boost investor confidence.

Conclusion

India’s growing dependence on steel imports, particularly from China, underscores the shifting dynamics of the global steel market. While imports help meet rising domestic demand, they also create challenges for local manufacturers. Balancing competitive pricing with sustainable growth for Indian steelmakers will require strategic government intervention and industry collaboration.

For all your metal fabrication needs, visit Lux Metal Group for customized solutions and state-of-the-art services.